Banking & Credit Unions

Management succession, documented before anyone asks for it.

Why succession planning is different in banking

Bank governance puts succession squarely on the board's desk. Examiners routinely ask how the board has addressed management succession, and directors are expected to show more than a discussion noted in last year's minutes. What reads well in that conversation is specific: critical roles identified, successors assessed against defined criteria, development underway, and a record showing the plan is reviewed on a cadence. What reads poorly is a plan assembled the month before the exam. The difference between the two is whether succession runs as an operating practice the rest of the year. Credit unions face the same question from their own examiners and boards, with the added wrinkle of member-elected governance.

Community banking is heading into a leadership transition wave. A generation of long-tenured CEOs and senior officers is approaching retirement, and in smaller markets the external candidate pool is thin to nonexistent: the executives who could run your bank mostly already run someone else's. That leaves internal development as the realistic path, and internal development runs on multi-year timelines. A commercial lender needs years of credit cycles, board exposure, and community standing before the CEO seat fits, which is why the 2 to 3 year readiness window is where most community bank succession work actually happens. Boards that start the internal build early keep the option of an external search; boards that start late take whatever the market has left.

Below the executive tier, the exposure gets sharper. Senior lenders hold relationship books that follow the person out the door if there is no continuity plan. Compliance and BSA officers are one-deep at many institutions, which turns a single resignation into immediate regulatory exposure. And finance leadership carries reporting cycles that do not pause for a search. These are the seats where key-person risk is concrete and datable, and where a bench mapped across readiness windows earns its keep.

The roles bank and credit union plans have to cover

Board attention goes to the corner office, but the vacancy risk is spread across a handful of seats the institution cannot run without.

President and CEO

The board owns this transition, and a credible internal candidate changes every part of it: the timeline, the search cost, and the conversation with the regulator. Building that candidate takes years, which is the argument for starting now. Readiness windows make the board conversation concrete: who could serve today, and who is two development years away.

Chief lending officer and senior lenders

Borrower relationships are the franchise. Succession here means planned continuity for the book: overlap periods, introductions made early, and a bench of lenders developed through real credit cycles rather than a scramble after the resignation. The 1 year window is often the right frame here, long enough for joint calls and a planned handover of the book.

Compliance and BSA officers

Often one person deep, always regulator-visible. A vacancy opens exposure the day it happens, so this seat needs named emergency coverage and a developing successor at the same time. Cross-training an analyst toward this seat is one of the cheapest risk reductions available to a smaller institution.

CFO and controller

Call reports, audits, and board packages run on a calendar that ignores vacancies. Finance succession is unglamorous and quietly urgent, and it is usually missing from the plan entirely. A scored successor with a stated window turns that gap into a managed item instead of an unexamined one.

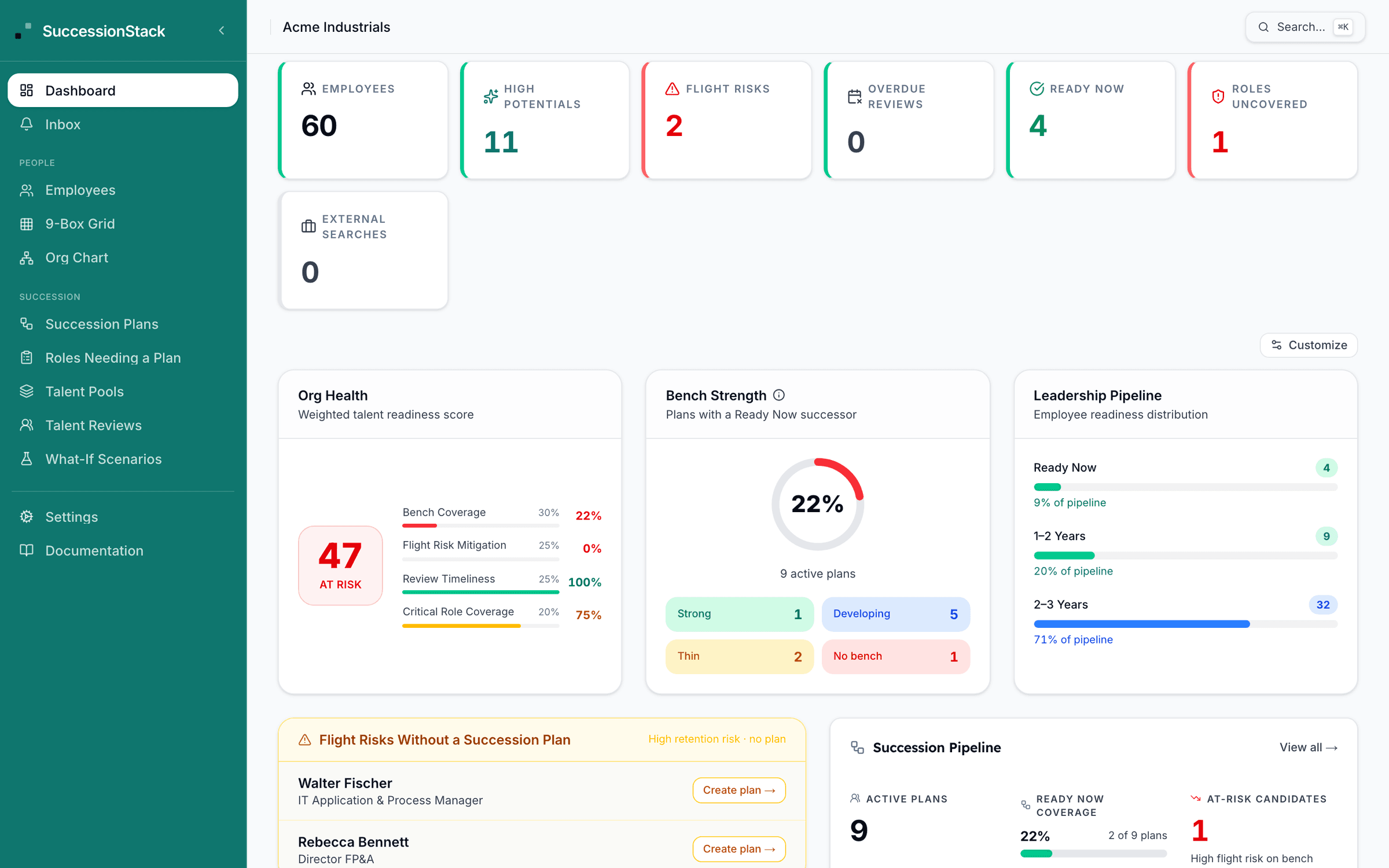

Bench strength the board can read.

SuccessionStack's analytics show bench strength, pipeline depth, and org health by function: which critical seats have Ready Now coverage, which are riding on a single 2 to 3 year candidate, and where the plan is thin. Directors get a view they can absorb in minutes, and because every score, weight, and plan change lands in an append-only audit log, the institution can show the plan and the discipline behind it, with dates. Pipeline analytics also show whether the lender bench is genuinely developing or merely listed, which is exactly the distinction an examiner probes.

How banks and credit unions get live

No core conversion, no integration project: a CSV and about two weeks.

Import the officer population

A CSV export from your HR system covers it. SuccessionStack runs alongside your HRIS rather than replacing anything.

Flag the regulator-visible seats

CEO, senior lending, compliance and BSA, finance, plus the branch and operations leaders you are one-deep on.

Score with role-adjusted weights

Eight dimensions, weighted differently for a chief credit officer than for a compliance lead, with every weight change logged.

Review with the board on a cadence

The plan becomes a standing committee item, and the audit log holds the exam-ready history without anyone rebuilding it.

Questions buyers actually ask

See where your bench breaks before it matters.

Bring your real org chart. We show you the succession gaps, cascade risks, and bench depth in a 30-minute walkthrough. IT security questions answered on the same call.

IT review first? The FAQs answer the security questions honestly →